Poland has quietly become Europe’s third-largest medical cannabis market, outpacing more mature systems like Italy and the Netherlands. But while its rapid growth is a remarkable success story, it’s also a cautionary tale about the risks of regulatory fragility—particularly for telemedicine. From a supply surge to a prescription collapse and partial recovery, Poland’s trajectory reveals the promise and perils of medical cannabis liberalisation without adequate guardrails. As other European countries, especially Germany and Australia, navigate their own telemedicine debates, Poland’s experience offers both warning signs and a model for adaptation.

Table of Contents

Unprecedented import and sales growth until the telemedicine ban

Poland’s medical cannabis market has taken off at breakneck speed, transforming from a niche sector into a rapidly scaling industry in just a few years.

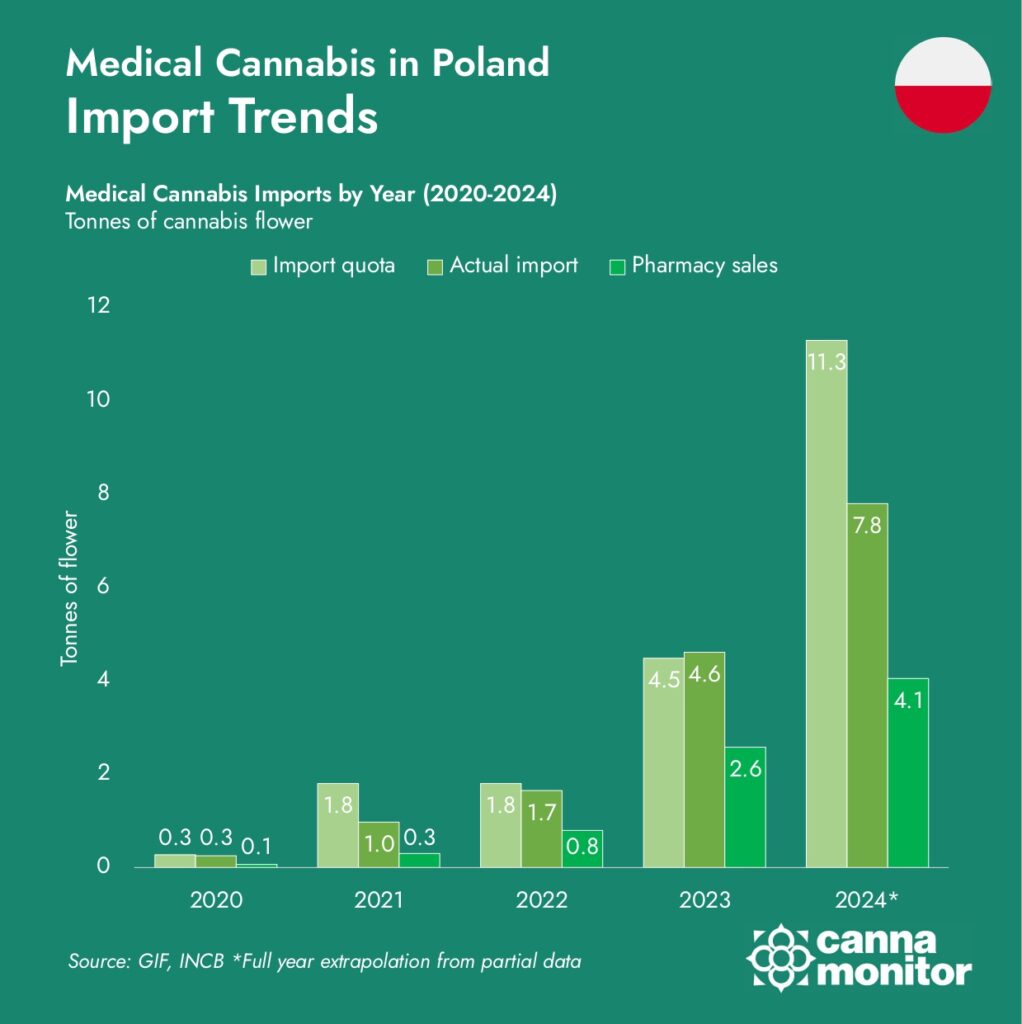

But from there, the momentum built fast; by 2021, import volumes more than tripled to 1.0 tonne, and by 2022 they had nearly doubled again, reaching 1.8 tonnes closely tracked by rising pharmacy sales. Then came 2023, marking a turning point: imports surged to 4.5 tonnes, while pharmacy sales hit 2.6 tonnes, reflecting a system finally hitting its stride. In 2024, the growth story turns exponential, with expected imports soaring to 11.3 tonnes and patient dispensation projected to surpass 7.8 tonnes.approved facilities, but companies are still ramping up operations.

Behind Poland’s fast-growing sales was an equally striking surge in cannabis imports. In just four years, official imports rose from 300 kilograms in 2020 to over 11 tonnes in 2024, outpacing patient sales and positioning Poland as a strategic destination for international suppliers. In parallel, the country’s import quota has risen steadily, following complaints by operators about limits in the issuance of import permits, many of which are not consistently fulfilled.

Medical Cannabis Imports to Poland

However, operators have often requested import permits without fully utilising them, preemptively securing quotas “just in case.” This practice has led to periodic exhaustion of available quotas mid-year, prompting authorities to raise the cap, first to 11 tonnes in late 2023 and again to 20 tonnes for 2025.

With its newly expanded quota, Poland is positioning itself not just as a participant in Europe’s medical cannabis sector, but as a leader in access, regulatory stability, and forward-looking development.

All current volume is sourced from abroad as domestic cultivation has yet to materialise in practice, as it remains authorised on paper in government-approved facilities, but companies are still ramping up operations

This expansion has been enabled by liberal prescribing guidelines, minimal restrictions on indications, and a vibrant private telemedicine ecosystem that allowed thousands of patients (especially in rural areas) to access treatment. For many, this was a game-changer. It democratised access to care and brought thousands of new patients into the medical system.

Actually, imports are catching up to official quotas, reflecting tighter coordination, better forecasting, and a healthcare sector more confident in prescribing cannabis treatments.

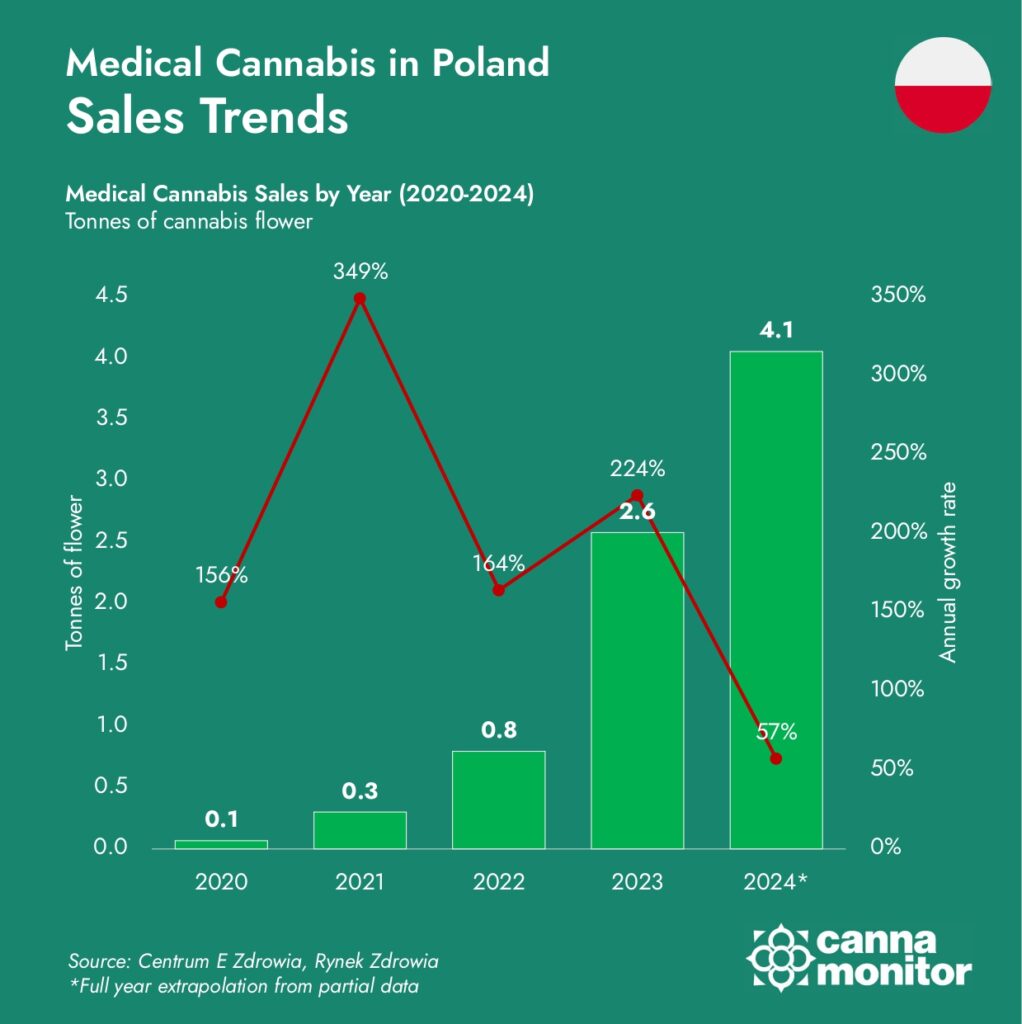

Pharmacy sales, once modest, have surged in parallel, rising from just 0.1 tonnes in 2020 to a projected 7.8 tonnes in 2024, confirming not only rising demand but genuine clinical integration.

This rapid alignment across policy, supply, and real-world usage points to a market that’s not just expanding; it’s maturing.

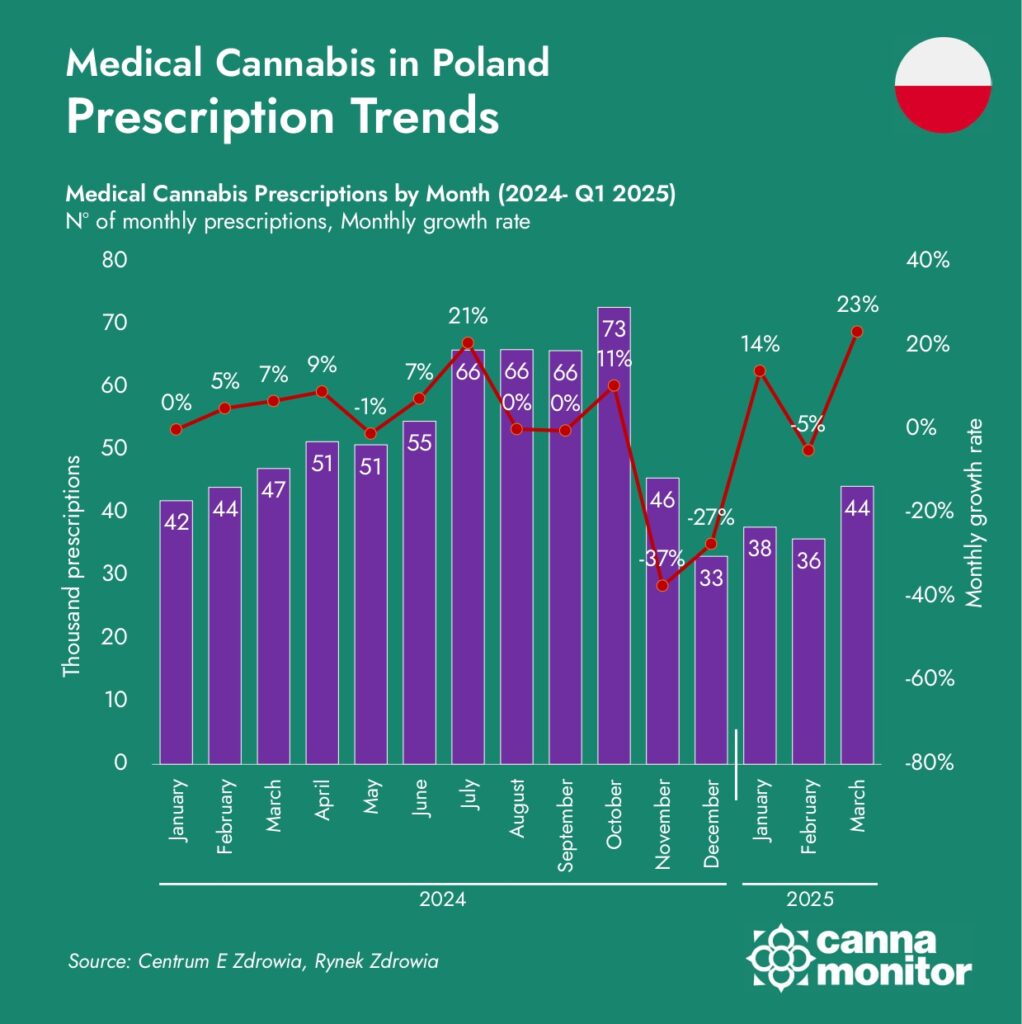

By late 2024, the infrastructure that drove access came under fire; A proliferation of so-called ‘receptomat’ platforms (automated or low-supervision online prescription services) sparked public concern and drew political scrutiny. In November 2024, Polish authorities imposed sweeping new regulations, requiring most prescriptions to be issued after an in-person examination.

The results were immediate; monthly prescriptions collapsed by 55%, falling from 73,000 in October to 33,000 by December. The crackdown (though framed as a compliance measure) disproportionately impacted patients in underserved regions and disrupted the progress made by Poland’s fledgling medical cannabis ecosystem.

All current volume is sourced from abroad, as domestic cultivation has yet to materialise in practice. With a 2025 import quota of 20 tonnes, Poland is asserting itself not merely as a player in the European medical cannabis sector, but as a frontrunner in terms of access, consistency, and progressive development.

Market rebounds: physical clinics, compliance and recovery

The sector responded with remarkable agility. By early 2025, operators began opening physical clinics and hybrid service models to comply with new requirements. These efforts began to bear fruit: by March 2025, monthly prescriptions had rebounded to over 44,000, up 23% from February, signalling that the system had begun to stabilise.

Behind the scenes, product diversity in Poland’s medical cannabis market is gaining remarkable traction. Despite the arduous product registration process taking over 1 year, more than 40 products (primarily flowers and extracts) have now received approval from over 20 suppliers, including leading international producers from Canada, Portugal, and Germany. Yet the variety available to patients extends well beyond what official registrations suggest.

Several companies strategically register a single cultivar or base product, then introduce multiple varieties of similar potency under the same licence, significantly expanding their commercial offerings while streamlining regulatory efforts.

Medical Cannabis Prescriptions in Poland

Licensed to prepare magistral formulations, Polish compounding pharmacies are increasingly seen as key innovators; some are moving beyond standard preparations to develop bespoke extracts, oils, and even vaporiser cartridges tailored precisely to physician prescriptions and patient needs.

This decentralised model fosters a highly responsive ecosystem, where new formats and potencies can enter the market with notable agility despite the highly-regulated nature of narcotics trade in the country. As regulatory processes gradually ease and the sector matures, Poland is shaping up to be one of Europe’s most dynamic and versatile medical cannabis markets, marked by fast adaptation, creative formulation, and growing therapeutic choice.

The effects of the regulatory shock continue to be felt. Trust has diminished, growth forecasts have been adjusted, and a sector once defined by innovation is now proceeding with greater caution. The transition from digital-first access to a more conservative hybrid model is likely to persist, at least until regulators are persuaded that robust standards can be introduced.

Poland’s next chapter: A lesson in sustainable growth and shared responsibility

Medical Cannabis Sales in Poland

Poland’s experience stands as a pivotal case study in the broader European debate over cannabis and telehealth. Like Germany and Australia, Poland allowed digital-first prescribing models to flourish, but failed to enforce clear standards around clinical protocols, advertising, and physician independence.

The result was predictable: political backlash, media scandals, and restrictive interventions that hurt patients as much as they punished bad actors. What was missing wasn’t necessarily regulation, but responsibility.

By the time rules were enforced, the damage was already done. In contrast, countries like Germany, despite mounting political pressure, still have time to avoid Poland’s fate by developing credible self-regulatory frameworks for telemedicine in cannabis care.

Despite recent setbacks, Poland’s market fundamentals remain strong; A large population, broad therapeutic guidelines, and increasing product availability provide fertile ground for renewed expansion.

However, the path forward requires a balanced approach; one that safeguards access while strengthening compliance. Operators must avoid reverting to risky shortcuts and instead focus on building clinic networks, enhancing physician training, and implementing strong compliance frameworks to restore trust in the sector. Policymakers, meanwhile, must differentiate between isolated cases of misuse and structural models that offer real healthcare value.

Poland’s experience highlights a broader truth relevant across Europe: access without accountability is unsustainable. Its rise and stumble offer a vital roadmap for countries at similar crossroads, showing that recovery is possible if industry actors lead the way in setting and upholding standards.

For Germany, Australia, and others, Poland serves as both a mirror and a cautionary tale. It demonstrates that telemedicine, while not inherently flawed, requires foresight and maturity to manage responsibly. Rather than banning certain access models, the focus should be on raising standards and ensuring professional oversight.

As prescription volumes recover and infrastructure develops, Poland has the potential to regain its status as Europe’s most dynamic cannabis market. However, its future will not be defined by deregulation or excessive control, but by a new model built on balance, trust, and shared responsibility.

The future of cannabis access is online; smart, balanced, and built to endure.