Germany’s pharmacy sell-out market surpassed €1 billion for the first time in 2025, with imports reaching a record 201.1 tonnes (+176% YoY) — making it the largest regulated medical cannabis market globally. This data brief examines the supply chain diversification that accompanied that growth, the regulatory and pricing pressures now reshaping the operator landscape, the wave of Canadian-led M&A and capital deployment that committed over €180 million in six months, and the three variables — patient acquisition velocity, supply corridor composition, and the MedCanG amendment — that will determine whether Germany sustains its trajectory in 2026.

Table of Contents

This analysis draws on BfArM quarterly import data (2018–2025), GKV-Gamsi reimbursement figures, company filings and investor presentations from over a dozen operators, and Cannamonitor’s proprietary calculations for sell-out estimates, country-of-origin breakdowns, and market sizing. Where official data is incomplete — particularly for patient counts, domestic production volumes, and private-pay pharmacy sales — we triangulate from industry surveys, platform disclosures, and secondary reporting, and flag uncertainty explicitly.

Record import growth in a diversified supply chain

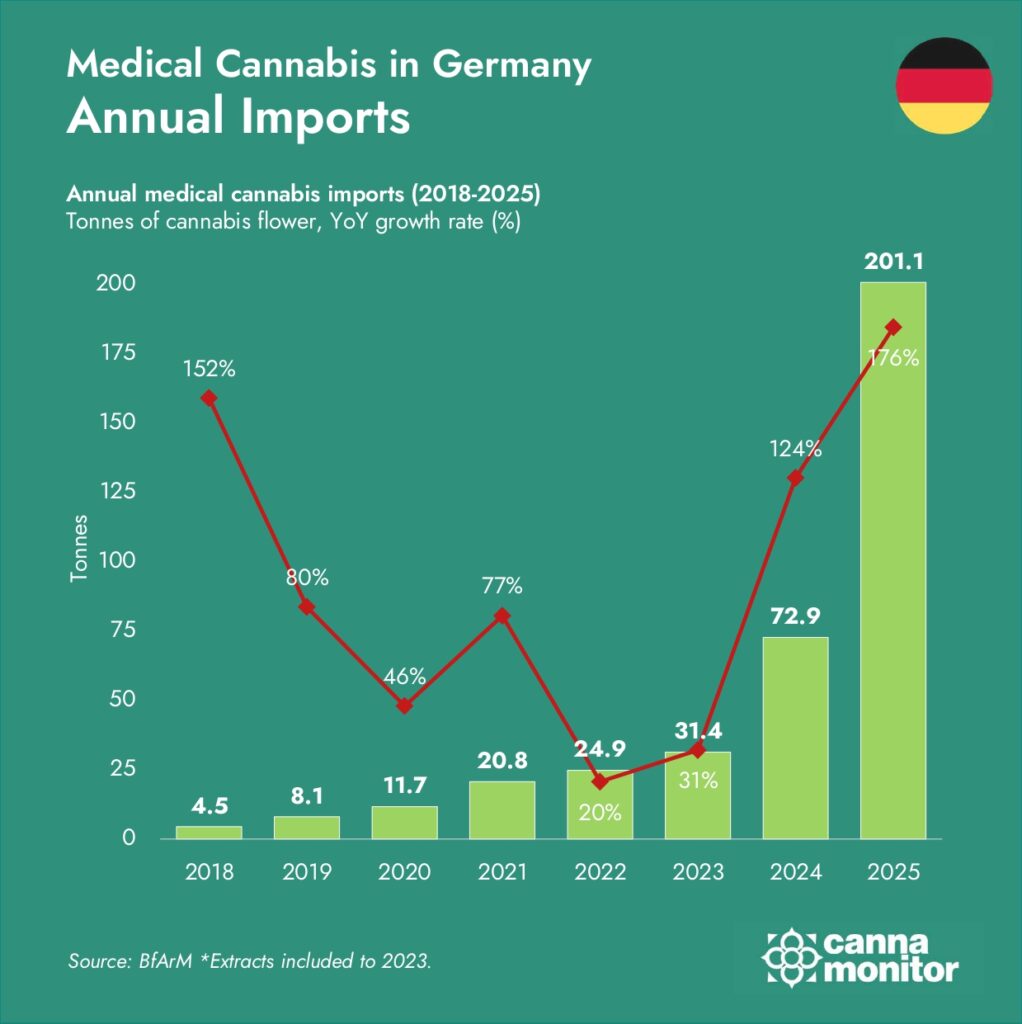

Germany’s import market nearly tripled in two years: 32.5 tonnes (2023) → 72.9 tonnes (2024, +124% YoY) → 201.1 tonnes (2025, +176% YoY). This is the largest annual volume any regulated import market has recorded.

The eight-year trajectory captured in BfArM’s quarterly release data illustrates three distinct phases: modest growth through 2022 under narcotics-law constraints; an inflection in 2023–2024 as reclassification unlocked new prescriptions and streamlined import procedures; and explosive scaling in 2025 driven by telemedicine platforms, accelerating patient onboarding, and supply chain expansion outpacing regulatory caps.

The estimated patient count reached ~900,000 by mid-2025, up from ~250,000 at the passage of the Cannabis Act (CanG) in April 2024, with projections ranging up to 1.4 million by 2027. Organigram’s investor presentation cited a German medical cannabis market valued at over €2 billion in 2025, with a forecast to surpass €4.5 billion by 2028. Cannamonitor’s own estimate is more conservative: >€1 billion in pharmacy sell-out for 2025.

Supply chain disruptions accelerated corridor diversification

The Canada–Portugal–Germany “triangle” that dominated 2024 fractured into a more distributed network in 2025. Multiple supply-side disruptions converged in H2:

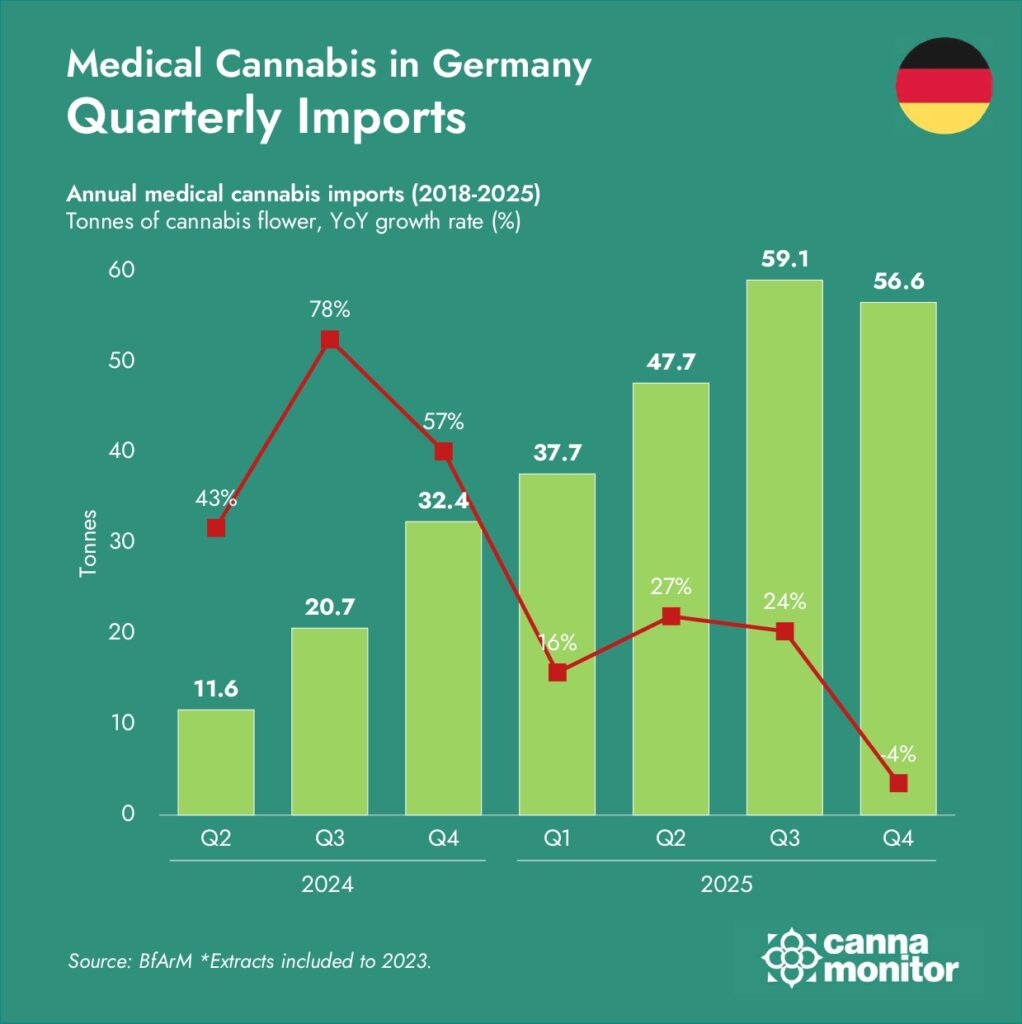

- The INCB import quota was exhausted mid-2025 at 122 tonnes, temporarily pausing all import permits. BfArM raised the cap to 192.5 tonnes in October 2025, but actual imports exceeded even the revised cap at 201.1 tonnes, requiring further re-estimation for 2026.

- INFARMED enforcement in Portugal — including Operations Erva Daninha and Ortiga and tighter certificate requirements that doubled approval timelines — added friction to the dominant processing corridor.

- Pre-restriction stocking and competitive price dynamics among distributors created demand pull-forward, amplifying Q3 volumes and contributing to the Q4 correction.

Annual medical cannabis imports (2018-2025)

Quarterly medical cannabis imports (2024-2025)

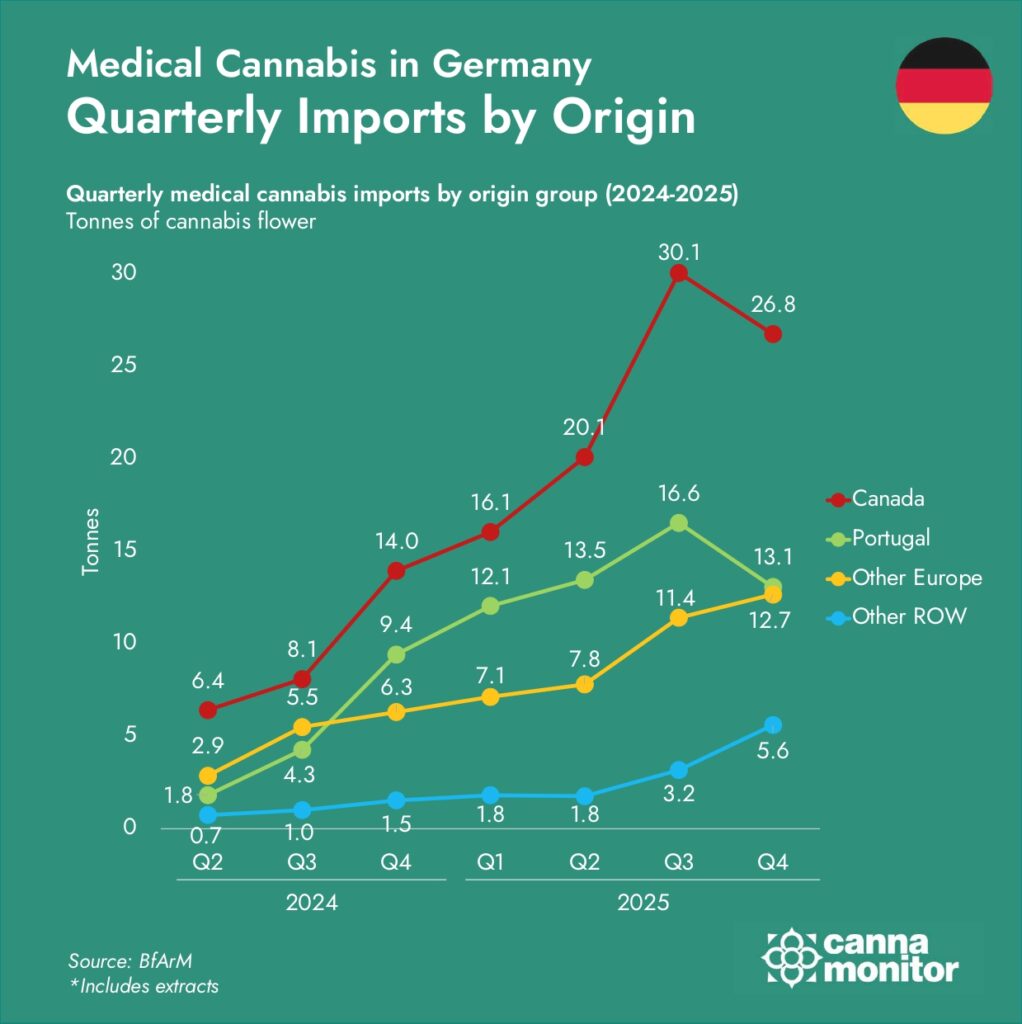

Medical cannabis imports to Germany by country of origin (2022-2025)

Medical cannabis imports to Germany by country of origin (2022-2025)

Medical cannabis imports to Germany by country of origin (2022-2025)

These disruptions reshaped the origin mix through three visible effects:

Canada’s direct share increased from 40% to 49%. Canada shipped 93 tonnes directly to Germany (+181% YoY) — roughly half of all imports — as firms increasingly bypassed Portuguese processing. Between H2 2024 and H1 2025, approximately 25 tonnes of Canadian product still flowed through Portuguese EU-GMP facilities, but the shift to direct supply accelerated sharply in H2.

Alternative European hubs emerged. Malta surged to 4.9 tonnes (+2,900%) from near-zero in 2024. Czechia contributed 4.7 tonnes (+261%), heavily concentrated in H2. The United Kingdom reached 3.6 tonnes (+1,001%) in a largely unexpected jump. Established suppliers — Denmark (9.3t, +26%), North Macedonia (8.2t, +207%), and Spain (4.8t, +117%) — held their positions.

Non-European origins surged in Q4. Australia shipped over 4 tonnes (2+ in Q4 alone), its best export year. South Africa reached 3.7 tonnes (+252%) and Colombia 3.5 tonnes (+447%), both accelerating sharply in Q4 as supply chains diversified beyond Europe and North America.

Portugal still shipped 55 tonnes (+220% YoY), remaining the clear second supplier — but its H2 deceleration after the enforcement actions signals a structural shift. Germany now sources medical cannabis from more than 25 countries, a level of supply diversification unmatched by any other regulated import market.

€1 billion in sales under regulatory and pricing pressure

Factoring in re-exports, processing losses, and regulatory clearance lag, as much as 120-160 tonnes of the 201.1 tonnes imported are estimated to have reached patients — a sell-through rate of 70%, up from approximately 60% before reclassification. This translates into pharmacy sales exceeding €1 billion for the first time, overtaking Australia as the largest regulated medical cannabis sell-out market globally.

MedCanG amendment: the single largest binary risk

The proposed MedCanG amendment could significantly constrain future growth. Health Minister Nina Warken (CDU) published the draft on 14 July 2025, proposing mandatory in-person consultations, a mail-order ban for cannabis flowers, and elevated penalties for non-compliant prescribing. The Cabinet approved the draft on 8 October 2025, with the Bundestag’s first reading held on 18 December 2025. A parliamentary vote is expected in April 2026.

The SPD categorically opposed the draft. Lawmaker Carmen Wegge stated: “We will not support the draft law in its current version under any circumstances.” With the CDU holding only 328 of 630 Bundestag seats, legislative gridlock is likely. A survey of 9,583 patients by MedCanOneStop found that 92.6% fear recriminalisation and 59.2% would switch to illicit sources if digital access is blocked.

If telemedicine and mail-order are restricted, Cannamonitor estimates the addressable market could shrink by up to 50%, given that cannabis platforms (DrAnsay, Bloomwell, CanDoc) generated the majority of new patient volume in 2025. The net political read: medical cannabis retains bipartisan protection. The CDU frames it as a healthcare issue rather than a drug policy issue — a notable rhetorical shift. The principal risk lies in the pace of further liberalisation rather than outright reversal.

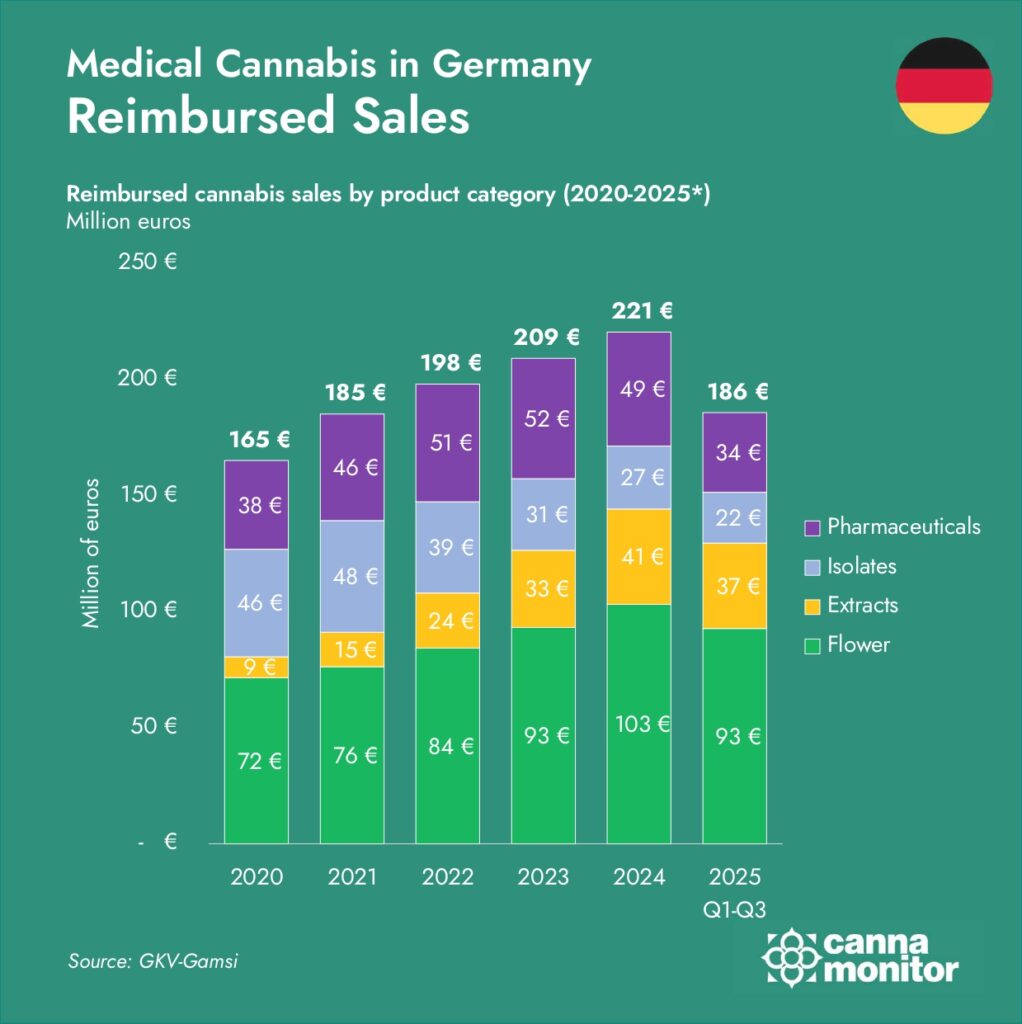

GKV reimbursement under pressure

Approximately 20% of total pharmacy sales are reimbursed by Germany’s statutory health insurance system (GKV), on track for over €200 million in covered products — predominantly flower and full-spectrum extracts, as dronabinol sales stabilise.

The Federal Ministry of Health (BMG) has cited the divergence between rising import volumes and comparatively slow GKV prescription growth as evidence of recreational abuse. Health insurers are openly considering stopping reimbursements for cannabis flower altogether — a move that would redirect approximately €200 million per year and reshape demand toward extracts and oral formulations.

GKV-reimbursed medical cannabis sales

A maturing operator landscape across 1,500+ SKUs

Price compression has accelerated in the last quarters. The average pharmacy gram price has fallen from barely €10 at the time of reclassification to closer to €6 — a 40% drop in under two years. Yet the market is segmenting, not collapsing: discounted flower now retails for as little as €1 per gram, while premium genetics and novel formulations still command prices above €10. Across over 1,500 SKUs, the spread is widening rather than narrowing. The pattern mirrors what mature cannabis markets in Canada and Australia have already demonstrated: rapid SKU proliferation erodes margins for undifferentiated producers, forces consolidation among mid-tier operators, and rewards the few with brand recognition or vertical cost advantages.

The €1 billion market is now served by a growing number of operators with increasingly visible financials.

- Four20 Pharma (majority-owned by Curaleaf, which reported record Q4 2025 international revenue of $51M, +65% YoY) is estimated at ~€100M in revenue and holds >10% market share.

- Cantourage, the largest publicly listed German operator, reported ~€75M in 9-month 2025 revenue (+148% YoY) and is on track for €5.5–6.5M in full-year EBITDA.

- Remexian (~C$100M annualised revenue, ~15% market share, 200+ SKUs from 19 source countries) was acquired by Canada’s High Tide at 3.6× EBITDA.

- Sanity Group reached €60M in 2025 revenue before being acquired by Organigram for €113M upfront, with total consideration of up to €227M including earnouts. Its medical brand avaay is claimed as the #2 in German pharmacies.

- Enua roughly tripled revenue to an estimated €40–50M and secured a €25M Deutsche Bank credit facility — the first tier-1 European bank cannabis debt in Europe.

- Grünhorn, which claims ~20% market share and has grown its patient base 146% YoY, launched the CanDoc telemedicine platform in 2025.

- Tilray operates through CC Pharma, which posted a record $85.3M distribution quarter in Q2 FY26 with international cannabis revenue growing 36% YoY, leveraging its original BfArM cultivation licence.

- Canopy Growth, which reported C$6.2M in Q3 FY2026 international cannabis revenue (+22% sequentially as European supply chains improved), distributes in Germany through Cansativa, the exclusive partner for its Tweed brand.

- Demecan, the only fully vertically integrated German operator, raised €100M — the largest European cannabis equity raise — and is doubling cultivation capacity to 4,000 kg/yr.

- Aurora, another original BfArM licence holder, reported record international medical revenue of $48M in Q3 FY26 (+17% YoY) and is expanding its Leuna facility for domestic EU-GMP output.

- IMC (via Adjupharm) generated C$23.3M in 9-month 2025 Germany revenue (+122% YoY), though the parent company flagged a going-concern note amid margin compression.

- Weeco (acquired by SynBiotic SE, which guides ~€26M consolidated revenue for FY2025) is SynBiotic’s largest revenue contributor.

- On the demand generation side, telemedicine platforms drove the majority of new patient volume: DrAnsay alone moved 1,859 kg through partner pharmacies in January 2025, while Bloomwell published data showing a 3,300% prescription surge between March 2024 and December 2025.

Product innovation expanded meaningfully beyond flower in 2025: Demecan launched the first EU-GMP live rosin extract; Curaleaf International achieved EU certification for a handheld liquid inhalation device; Grünhorn launched a medical cannabis cream for chronic skin conditions; and Vertanical’s VER-01 — a full-spectrum cannabis extract for chronic low back pain — passed a Phase 3 randomised controlled trial showing superiority over opioids, potentially becoming the first whole-plant cannabis medicine with EMA-equivalent approval.

Domestic production and capital deployment

Local production is ramping but remains structurally marginal. Germany imported over 30 times what it produced domestically, making the gap between cultivation and consumption among the widest in any regulated market. The three authorised producers — Aurora, Demecan, and Tilray (formerly Aphria) — had a combined capacity of up to 2.6 tonnes per year under the original BfArM tender. With the liberalisation of cultivation under MedCanG, all three announced expansions.

Demecan announced capacity doubling to 4,000 kg/yr and separately raised €100 million — the largest single European cannabis equity raise. Four new cultivation licence applications were filed as of October 2025, including German Cannabis Standards, which announced a €10 million financing round to build a 21,000 sqm facility in Bitterfeld-Wolfen. Germany’s medical cannabis exports dropped 21% to 5.9 tonnes — confirming that Germany remains overwhelmingly a demand market.

Three Canadian-led acquisitions in rapid succession (September 2025 – February 2026) deployed nearly €200 million into European cannabis, with Germany as the primary target.

The 2.4×–12.6× EBITDA spread across the three acquisitions reveals fundamentally different bets on Germany’s regulatory trajectory. Organigram acquired Sanity Group for up to €250 million including earnouts — the largest cross-border cannabis deal targeting Europe since Curaleaf’s acquisition of EMMAC in 2021 — pricing in brand equity and recreational optionality. BAT (British American Tobacco) invested C$65.2 million in Organigram equity to finance the cash component. High Tide took a measured 51% stake in Remexian — Germany’s largest distributor by volume (~15% market share, 200+ SKUs) — at 3.6× EBITDA, reflecting a distribution-first strategy. Cronos Group acquired Netherlands-based CanAdelaar for €57.5 million at 2.4× EBITDA, securing GMP infrastructure and exposure to the Dutch Wietexperiment. Enua’s Deutsche Bank facility is a landmark: the first time a tier-1 European bank has extended a cannabis credit facility, signalling growing institutional comfort with cannabis cashflows.

Germany at a crossroads: 2026 outlook

If H2 2025 trends hold, Germany is on track for 220–240 tonnes of imports in 2026. The trajectory depends on how three variables resolve.

- Patient acquisition velocity. If telemedicine access is preserved, the current ~900,000 patient base could approach 1.2 million by year-end, sustaining volume growth even as per-patient spending stabilises.

- Supply corridor composition. The enforced diversification toward Malta, Czechia, and direct Canadian shipments creates a more resilient but potentially less price-competitive supply chain. Whether the Q4 surge from Australia, South Africa, and Colombia represents sustainable corridors or one-off stockpile clearances will become clear with Q1 2026 data.

- Regulatory developments. The MedCanG amendment vote expected in April 2026 represents the single largest binary risk — restrictions on telemedicine and mail-order could compress the addressable market by up to 50%, while a watered-down compromise would leave the growth trajectory largely intact. A separate threat — potential GKV exclusion of flower reimbursement — would redirect ~€200 million annually and reshape demand composition toward extracts and oral formulations.

Domestic production is unlikely to become material before 2027 at the earliest, even with Demecan’s 4-tonne target and Aurora’s Leuna expansion. Germany will remain structurally import-dependent for the foreseeable future — and the commercial bet on continued growth is now substantial.

Germany has set a new global standard for what a regulated cannabis market can become — data-driven, medically anchored, and commercially viable. The challenge now is to sustain this momentum while navigating a shifting political terrain and maturing market dynamics.